Capital Crusaders on the March

Capital crusaders have widened their international presence; 40% of the campaigns are in countries including Russia, South Korea, and Switzerland [JP Morgan]. Photos courtesy of Getty Images.

Capital crusaders have widened their international presence; 40% of the campaigns are in countries including Russia, South Korea, and Switzerland [JP Morgan]. Photos courtesy of Getty Images.

Written by Yana Sinkevich

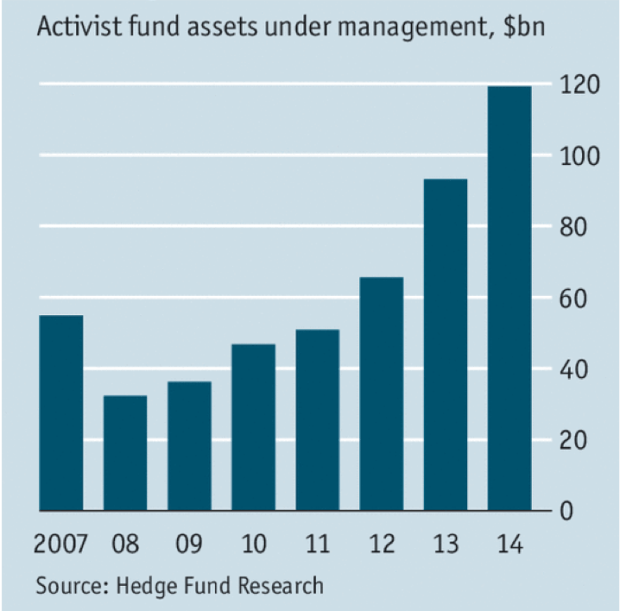

The corporate raiders are back. Since the Global Recession, investors have piled into activist hedge funds searching for alpha or excess returns benchmarked against the market. The growth of these professed “protectors of capital” is unsurprising given the extreme global losses experienced during the 2008 financial crisis.. Activist fund assets under management (AUM) have increased over 325% since 2009, with a nominal value pegged at approximately $121.8B in Q3 2015.[Source: JP Morgan, Business Insider]

Capital crusaders have widened their international presence; 40% of the campaigns are in countries including Russia, South Korea, and Switzerland [JP Morgan] The frenzy around activist investors is also prevalent in the media. Prominent on front pages of newspapers and on TV screens are titans such as Carl Icahn who recently called for a three-way split of AIG, and Bill Ackman who continues to defend Valeant amid fraud allegations in hopes of stabilizing its share price amid a selloff.

Icahn, Ackman and other knights of shareholders’ equity seek to unlock value within target firms. They acquire typically 5% ownership and purchase additional call options or rights to buy shares that are exercised if their campaigns are well received. Their tactics range from friendly letters to CEOs that highlight criticism and solutions to hostile proxy battles where activists co-align with other shareholders to establish new management via proxy votes.

At every campaign’s core is a disagreement regarding a firm’s organizational strategy. Grievances range from insufficient leverage for generating adequate capital returns to poor corporate governance practices. The most popular form of hedge fund activism seeks to split up a company or to divest business lines or other assets as in Icahn’s proposal for AIG. By influencing or poaching seats on the board, activists are able to enact share buybacks or dividend payouts which apply upward pressure on share price. Activists can also broadly improve efficiency to boost performance, which drives up share price as well.

When they complete their campaigns and exit, activists collect enormous returns from this share value creation. This may sound similar to private equity; however activist hedge funds purchase minority ownership stakes and have much shorter investment horizons. There is no intention to take target companies private to later spin them off.

The influence of activist hedge funds has transformed dramatically over the years due to technology, particularly involving social media. Today, even one percent ownership warrants attention from management, compared to the historical 5% ownership and subsequent SEC 13D registration, in which an activist communicates campaign proposals.

With just a click of a button on Twitter, Icahn has ignited Apple stock rallies by declaring the company undervalued. Furthermore, after Icahn tweeted earlier this year that he had fully exited his Netflix position, he raked in a campaign profit of $1.6B before driving the share price down by 4% [Bloomberg]. Activists will also frequently engage target firms, shareholders, and other market players using their own homepages.

Apple, which has the largest public market capitalization, is also being targeted by Quarz Capital. The firm has called for a separation of software and hardware operating results in its financial reports to increase transparency and perception of Apple as a software company. Both Quarz Capital’s and Icahn’s initiatives would allegedly increase share price; however management hasn’t complied with these requests [BIDNESS ETC].

Nelson Peltz — who purchased Snapple from Quaker Oats Co. for a mere $300MM before bundling it in a portfolio and selling it to Cadbury for $1.45B a few years later — recently announced his $2.5B ownership purchase of General Electric Co [The Wall Street Journal]. Larger companies typically require greater ownership for an activist to make a meaningful managerial impact and are less receptive to campaigns. They are also more exposed to a wide range of institutional investors and as a result, characteristically exhibit leaner operations than those of smaller firms. Activists, however, are indiscriminate and have envisioned untapped value at large, well managed companies in the past. In short, scale does not protect firms from these crusaders.

“Activist have come a long way from the early 1980’s when they were despised by Corporate CEO’s and large institutional investors,” said Professor Charles Murphy who teaches the Investment Banking: The Financial Services Industry course at NYU Stern, “Today they are widely accepted as disruptors who seek to make changes to the companies they interact with. With more investor sentiment in their favor, today’s CEO can’t afford to ignore them.”

On average, activist strategies have beat other hedge fund strategies by 99 basis points or 0.99% over the past 5 years [Prequin]. Target firms generally experience a surge in share price before the announcement of the activist campaign based on rumors that circulate while the activist slowly accumulates shares. A public announcement of a campaign permanently increases share price by 210 basis points within one day on average. The majority of activist hedge funds have an average investment horizon of six months, however target firms continue to generate alpha returns five years after the inception of the activist campaign. Returns on a peer-by-peer basis, however, are volatile with over 30% of hedge fund activists underperforming the market [Source: JPMorgan, ValueWalk].

Despite their adoration by investors, hedge fund activists face harsh criticism for questionable practices and misrepresented performance. “Activist shareholders generally provide a free service to all passive shareholders by disciplining management,” said Yakov Amihud, the Ira Rennert Professor of Entrepreneurial Finance at NYU Stern. “But I cannot say that the strategies which they press management to carry out — e.g., sale to another firm, splitting the firm, de-staggering the board of directors — are always superior to those that management support. They are often wrong, partly because they do not have all the information that management has. And, sometimes they are just stock pickers, not really activist shareholders. Perhaps their most valuable role is in the threat they pose to lazy and self-serving management.”

The question of morality among activist hedge funds stretches beyond the aggressive nature of their work. Bill Ackman currently faces an insider trading lawsuit. The activist allegedly knew Allergan planned a takeover bid for Botox and purchased shares of the pharmaceutical company leading up to the public announcement.

Although activist hedge funds have experienced losses this year due to global market volatility, the likes of Ackman and Icahn are here to stay. The business model for activism is both effective and efficient, requiring credibility and little capital. The business model is a stark contrast to private equity funds that typically require larger capital contributions and longer investment horizons. It is the perfect blend between private equity and hedge funds, allowing for quick entry and exit, which investors seek.

The macroeconomic, too, has and will continue to encourage activist campaigns. Rates are low, and while they are expected to rise marginally, the cost of credit will likely remain inexpensive on a historic basis. Cheap credit will allow activists to continue financing their campaigns with ease. Additionally, activists’ journeys into foreign countries make for tremendous possibilities, particularly in a time when corporations are conservative. With cheap debt and investors piling into their funds, activists have a plethora of opportunities to target companies and stretch their balance sheets to their limits for returns.

Corporations beware: Very little stands in the way of these crusaders of capital.

Leave a comment