Bankers vs. Mattresses: The New World of Negative Interest Rates

Warren Buffett explains that “interest rates are like gravity on asset valuations,” as rates drop stock valuations continue to be priced artificially high. Photo courtesy of The Wall Street Journal.

Warren Buffett explains that “interest rates are like gravity on asset valuations,” as rates drop stock valuations continue to be priced artificially high. Photo courtesy of The Wall Street Journal.

Written by Tim Udelsman

NIRP? ZIRP? ECB? BoJ? QE? It’s no secret that the modern world of interest rates and central bank monetary policy is confusing. According to standard economic theory, manipulation of interest rates on sovereign debt allows central bankers either to stimulate economic growth or to stave off potential recessions. While this has been typically the goal of monetary policy for over a century, its use today is very different than it was before.

Central bankers reserve the ability to alter their country’s money supply, thus raising or lowering interest rates according to changes in the macroeconomic environment.

Previously, a widely-held belief prevailed that the lowest that interest rates could go to was 0 percent, the hypothetical lower bound. Yet, in recent years this boundary has been blurred as the European Central Bank (ECB), Bank of Japan (BoJ), and others have adopted a negative interest rate policy (NIRP).

What does this mean? With negative interest rates, banks pay to store their reserves in a central bank rather than receive interest. Thus, holding money with the country’s central authority degrades the value of assets over time. For example, a commercial bank in Europe that deposits $1 billion of customer assets through the ECB, charging a -0.4 percent deposit rate, will incur a $4 million charge annually.

While negative interest rates are not currently being passed onto consumers but instead being absorbed by commercial banks themselves, the rates still beg an interesting question: Why don’t banks withdraw their electronic deposits from central banks and store them in vaults to avoid fees? The answer is that the costs of withdrawing, storing, counting, moving, and insuring are greater than the costs incurred in storing them in the central bank. Original theory suggests that negative interest rates incentivize commercial banks to withdraw funds from the central bank and lend to consumers, rather than incur costs to hold them with the central bank. Despite this theory, there is little proof that commercial banks are adopting this strategy.

While negative interest rates may seem unprecedented, other countries have effected negative rates before. Switzerland implemented negative rates in 1970s to counter currency appreciation while Sweden and Denmark used the same tactics in 2009 and 2012 to counter “hot” capital inflows which originate from foreign investors and can cause economic instability. However, the difference now, is the broad scope of its usage. To spur economic growth, the ECB initiated negative rates in 2014 while the BoJ, in a country that has been reeling from deflation and stagnant growth for decades, started in 2015.

So, where does that leave us today? Currently, over $13.4 trillion in outstanding negative yielding sovereign debt, up nearly 15 percent from just a few months ago, is sitting across global financial markets in the hands of institutions and investors. Central banks continue to tie up more of their countries’ wealth – the BoJ’s balance sheet has reached as far as 90 percent of Japan’s GDP. Meanwhile, growth across the Eurozone has remained stagnant, and Japan continues to miss its inflation targets. Criticism has been sharp – Warwick University Professor Emeritus of Political Economy Robert Skidelsky describes negative rates as “a desperate measure by governments that can think of nothing else to do.”

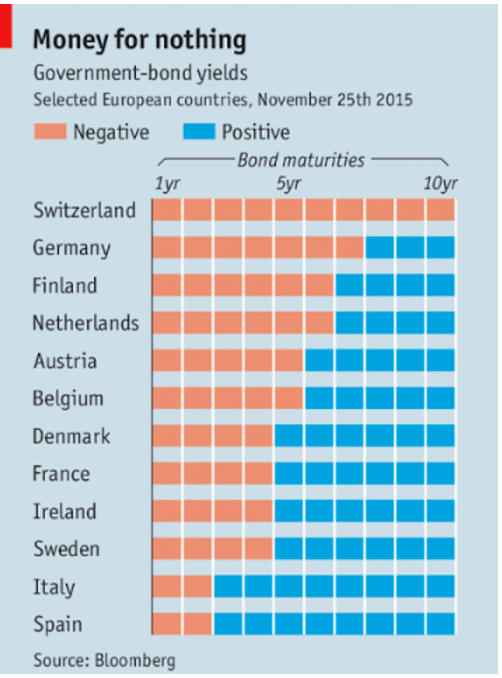

Chart showing the range of negative yielding debt available across the Eurozone and how long the negative yielding debt can extend. Photo courtesy of The Economist.

Despite the questionable effectiveness of NIRP, tying up such a large amount of money and artificially lowering rates to such an extent can lead to immense risks. The most prevalent risk is the possibility of another asset bubble. Warren Buffett explains that “interest rates are like gravity on asset valuations,” as rates drop stock valuations continue to be priced artificially high. Furthermore, as sovereign debt yields have been so low, investors have been piling onto higher yielding, riskier debt in search for returns. If government yields return to normal levels, investors could flee this risky debt and cause prices to collapse, creating volatility and financial damage.

Where interest rates will go and what moves central bankers will take next in an effort to jumpstart their economies are unclear. What we do know is that an enormous amount of negative yielding debt continues to grow as more money gets tied up in this experiment in monetary policy. Whether this accumulation of negative yielding debt leads to massive economic revival, a devastating economic bubble, or something in between, this unprecedented monetary policy is sure to make history.

Leave a comment