Spotify’s IPO: What You Need to Know

Courtesy of The Hill

Courtesy of The Hill

Written by Alexis Datta

Spotify is one of few companies that has done a direct listing for a few reasons. First, it has a large amount of cash reserves and did not need to raise money by way of its IPO. Second, it targeted all investors, not just a handful, and its strong brand recognition helped to garner interest.

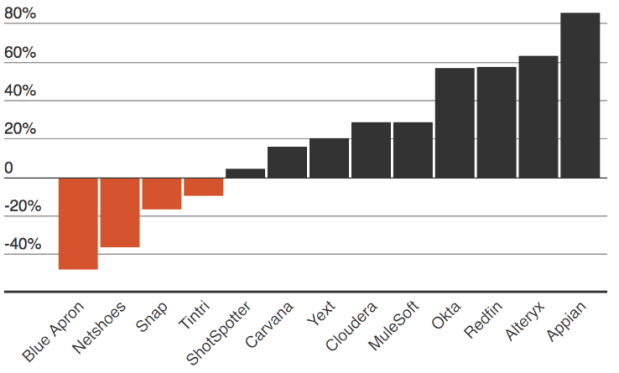

Spotify, the popular music streaming platform, announced its initial public offering (IPO) earlier this year. Spotify’s IPO follows in the footsteps of a few big-tech IPOs that took place in 2017, including Blue Apron, Snapchat, MuleSoft, and Redfin. Software development tools company Pivotal Software and e-sign platform DocuSign will follow suit later in the year and have announced IPOs as well. With the Spotify IPO hinging on a non-traditional stock distribution called a ‘direct listing’, there are a few things you may want to know.

Spotify’s Debt Covenants

In 2016, in order to compete against the then-newly introduced Apple Music, Spotify took out a $1 billion private loan from Goldman Sachs, TPG, and Dragoneer. Because investors and Spotify diverged in opinion on company value and repayment ability, the firms placed debt covenants that mandated the IPO that was recently announced. Debt covenants are agreements that delineate requirements on which borrowed capital is contingent. In Spotify’s case, the company had to sign off on an agreement that forced it to go public and allowed investors to convert their debt stakes into equity at a discount. As a move to ensure the profitability of the investment, the covenants act as a signal of investors’ low confidence, which are exacerbated by Spotify’s issues in generating revenue. Even though Spotify has more users than Apple Music – its primary competitor – most of Spotify’s customers use only the free service, and unlike Apple, Spotify has no other revenue-generating product lines.

‘Direct-to-Market’ IPO

Spotify bypassed the traditional IPO route, and did not enlist investment banks to perform normal IPO functions, such as finding initial buyers for the stock. Instead, the company listed its shares directly on the market, and allowed the market to decide its price. Spotify only published a suggested valuation that came from Morgan Stanley, one of three investment banks that Spotify did hire to perform administrative work for the listing. This move saved Spotify approximately $300 million in fees paid to banks primarily for underwriting, valuation and finding buyers. However, the direct-to-market IPO could have spelled trouble in three ways.

First, because the valuation was not directly contested since banks did not provide financing, Spotify could have maintained any of its previous valuations, which varied from the $8.5 billion valuation it received from private investors to the $20 billion valuation it received from a share swap with Tencent earlier in the year. Second, the company did not raise money via its direct listing, because its main purpose was to allow investors to cash out of the company. Third, an immediate Goldman, TPG, and Dragoneer sell-off could have discouraged future investments and made the price incredibly volatile. To succeed, Spotify needed to convince mutual funds and other institutional investors of the long-term profitability of the company.

The Trend of Tech IPOs

There is also something to be said about the number of technology IPOs that have been happening in recent years. These IPOs have a tendency to be (and to be perceived as) over-valued. Mainly, large initial influxes from private investors are often baked in to the IPO valuation, leading to inflated offering prices. Spotify was no exception to this rule – when it was rumoured to have a $10 billion valuation, investors thought it was overvalued, even though the stock listed around $26 billion.

The Bottom Line

Its successful direct-to-market IPO has prompted discussions of Spotify’s ability to become a trailblazer by foregoing the traditional equity capital markets (ECM) function at banks. The argument is that this move could aggravate the already declining ECM profits which currently account for a quarter of profits at major banks. However, investment banks aren’t worried just yet. Spotify is one of few companies that has done a direct listing for a few reasons. First, it has a large amount of cash reserves and did not need to raise money by way of its IPO. Second, it targeted all investors, not just a handful, and its strong brand recognition helped to garner interest. After the stock went public, the volatility of the price was larger than it would have been had an investment bank been buying and selling shares to help buffer initial sell-offs.

About 10 days after its direct listing, Spotify (SPOT:NYSE) is up almost 13%, and although it did see volatility, the stock is certainly one to watch going forward.

Leave a comment